What you'll find in this article:

Most banks and credit unions don't have a strategy problem — they have an alignment problem. When retail, IT, operations, security, and vendor management plan separately, technology becomes the thing that divides departments instead of connecting them. This article explains how banking silos form, what misalignment costs, and how financial institutions can build a shared roadmap that connects strategy to execution.

This article covers: how silos form inside financial institutions, what misalignment looks like in practice, why technology alignment is a business issue, how to break down silos, and when a Strategy Workshop makes sense.

Most banks and credit unions don't have a strategy problem. They have an alignment problem.

If you've worked through our strategic guide for banking executives, you know that department alignment is one of the ten questions worth answering before your next planning conversation. The challenge isn't setting the direction — it's getting every team moving in the same direction at the same time.

Executive leadership may have a clear vision for growth. Retail teams may know exactly where the customer experience is slowing down. IT may understand which systems are stable, fragile, outdated, or difficult to integrate. Operations may see where workflows create extra work. Security teams may know which systems need better visibility. Vendor management may see how many partners, platforms, contracts, and support relationships are being carried across the institution.

Everyone may be right.

The problem is that they are often right separately.

That is how silos form. Not because teams do not care. Not because leaders are ignoring the institution's goals. Silos usually form because each department is solving real problems from its own seat, with its own priorities, timelines, systems, and pressures.

Those goals should support each other. But when departments plan separately, technology can become the thing that divides them instead of the thing that connects them.

The Strategy May Be Clear, But Execution Gets Messy

A bank or credit union can have a clear digital banking strategy and still fail to execute it when departments aren't working from a shared plan. Clear direction at the top doesn't guarantee aligned execution at every level.

The board may support deposit growth. Executives may approve a branch transformation strategy. Retail leadership may want to shift staff from routine transactions to relationship-building. IT may be asked to support more automation, stronger cybersecurity, better integrations, and new digital tools. Operations may be told to reduce friction. Security may be expected to modernize cameras, alarms, access control, and monitoring without adding unnecessary complexity.

On paper, the strategy makes sense. Then execution begins.

- A branch technology project depends on IT capacity.

- A security upgrade creates data that operations could use, but no one builds the workflow.

- A new customer experience initiative requires staff adoption, but branch managers were not included early enough.

- A vendor solves one problem, but creates another support relationship.

- An ATM or ITM rollout works technically, but no one measures whether it changed staff behavior or customer access.

- A cash automation investment reduces transaction time, but staffing models stay the same.

That is where strategy starts to drift. The issue is not that the institution lacks tools. The issue is whether those tools are connected to a cohesive bank digital transformation strategy.

How Banking Silos Form Inside Financial Institutions

Banking silos form gradually through practical decisions — not negligence. Each department solves a real problem from its own seat, and over time those independent solutions create a disconnected operating environment.

A retail team needs a better customer experience. An operations team needs a faster process. An IT team needs a stable system. A security team needs a safer branch environment. A vendor offers a solution for one of those needs. The tool gets purchased. The project gets completed. The immediate problem improves.

Then another team does the same thing somewhere else.

Over time, the institution collects systems, platforms, vendors, dashboards, contracts, support workflows, and reports that all solve something, but do not necessarily work together. The result is a disconnected operating environment where:

The institution may still function. Customers may still get served. Branches may still open every morning. But underneath the daily routine, the organization becomes harder to operate. That hidden difficulty is expensive, directly impacting operational efficiency in banking.

What Misalignment Looks Like in the Real World

Misalignment rarely announces itself. It shows up in everyday moments that seem manageable in isolation — but compound into serious drag across locations, teams, and budgets.

Retail Banking Strategy and the Customer Experience Gap

A retail leader may want branch staff to spend more time advising customers, identifying needs, and supporting deposit growth. That goal makes sense. But if staff are still tied to routine cash handling, transaction processing, manual balancing, device issues, or disconnected workflows, the customer experience will not change much.

The strategy says "relationship banking." The daily workflow says "transaction processing." That gap has to be addressed before the customer experience can improve.

Why do banking departments become siloed? Banking departments often become siloed because each team solves problems from its own perspective. Retail, IT, operations, security, vendor management, and branch teams may all make practical decisions that work locally but create complexity across the institution when they are not connected to a shared roadmap.

Aligning Retail Banking Technology and IT Infrastructure

Effective IT infrastructure banking requires a balance between uptime and innovation. When retail teams want faster deployment, IT must evaluate risk within the broader retail banking technology framework.

Retail may see IT as slow. IT may see retail as impatient. In reality, both teams may be responding to valid pressures. The problem is that they are not always planning from the same roadmap.

Security Tools Collect Useful Data, But Operations Does Not Use It

Modern security systems can do more than record incidents. Video surveillance, access control, alarms, transaction-linked video, monitoring tools, and case management workflows can all provide signals that help the institution operate better. But if security data stays inside the security department, the value is limited.

Those are operational benefits, not just security benefits.

Vendors Overlap Without Clear Ownership

Vendor overlap can create friction across the entire institution. One vendor may support ATMs. Another ITMs. Another cash automation. Another alarms. Another access control. Another video. Another remote monitoring. Each partner may provide value — but if ownership is unclear, every issue takes longer to solve.

When the answers are unclear, teams spend too much time coordinating instead of solving.

Why Technology Alignment Is a Business Issue, Not Just an IT Issue

Technology decisions in retail banking affect every department's performance — not just IT. A branch technology choice changes staffing. A video system affects investigations and operational visibility. A cash automation tool affects transaction flow and balancing routines. A vendor platform affects compliance, cost, support, and reporting. If the decision affects the business, the business needs to be part of the planning.

The best technology conversations include the people responsible for:

- Strategy

- Retail delivery

- Branch management

- Operations

- IT infrastructure

- Security

- Risk

- Vendor management

- Facilities

- Customer experience

- Service and maintenance

- Financial performance

This does not mean every department needs to approve every detail. It means the institution needs enough shared visibility to avoid solving one team's problem by creating another team's burden.

The Hidden Cost of Banking Silos

Siloed technology creates costs that rarely show up as a single budget line — but compound across internal time, delayed projects, inconsistent execution, and underused technology investments.

More Internal Coordination

When systems and vendors are disconnected, teams spend more time coordinating. More emails, more meetings, more escalations, more status checks, more uncertainty. The institution may be paying for the same problem twice: once through the vendor invoice and again through internal time spent managing the issue.

Slower Strategic Projects

Retail growth initiatives often depend on IT, operations, security, facilities, vendors, and front-line adoption. If those teams are not aligned early, projects slow down during execution. A stalled ITM deployment, micro-branch pilot, cash automation project, or video banking initiative can delay the business outcome the institution was trying to create.

Inconsistent Branch Execution

When each branch solves workarounds differently, the customer experience becomes inconsistent. One branch may promote ITM usage. Another may avoid it. One location may document incidents clearly. Another may rely on informal communication. Inconsistent execution weakens the strategy.

Higher Support Burden

Disconnected tools increase the support burden on IT, operations, branch managers, and vendor management teams. Even when outside vendors provide support, internal teams still need to manage access, explain issues, track follow-up, confirm resolution, review reports, and communicate with affected locations. A better support model should reduce internal burden, not simply shift it around.

Lower Return on Existing Technology

Many banks and credit unions already own technology that could produce more value. The issue is not always missing capability — sometimes the institution has not connected existing capability to the right operational use case.

- A video platform may support more than incident review.

- An ITM may support more than extended transaction access.

- A cash recycler may support more than faster balancing.

- A service portal may support more than work orders.

- An access control system may support more than door security.

Technology produces better returns when teams understand what it can do and how it supports the institution's goals.

Integrating Retail Banking Strategy and IT Infrastructure

Retail strategy and IT infrastructure share more planning dependencies than most leadership teams account for. The following areas require shared visibility — not separate workstreams.

ATM and ITM Strategy

ATMs and ITMs should be part of the institution's retail delivery model, not just equipment in the field. Leadership should know which transactions should move to self-service or assisted-service channels, which locations need extended access, how uptime affects customer experience, and how the fleet supports deposit growth, staffing, and market reach. If retail owns the experience and IT owns the infrastructure, both teams need the same plan.

Cash Automation

TCRs, cash recyclers, counters, and related cash handling tools can reduce manual work, improve balancing, strengthen controls, and free staff time. The value depends on how branches actually use them. A cash automation project should include retail, operations, IT, security, branch management, and training — otherwise the tool may be installed without changing the workflow enough to improve efficiency.

Digital Video Banking

Digital video banking can expand service access and support more flexible branch models, but implementation requires more than customer-facing technology. Teams need to align on staffing, scheduling, escalation, connectivity, privacy, customer adoption, physical placement, signage, support, and measurement. If those details are handled separately, the experience can feel fragmented.

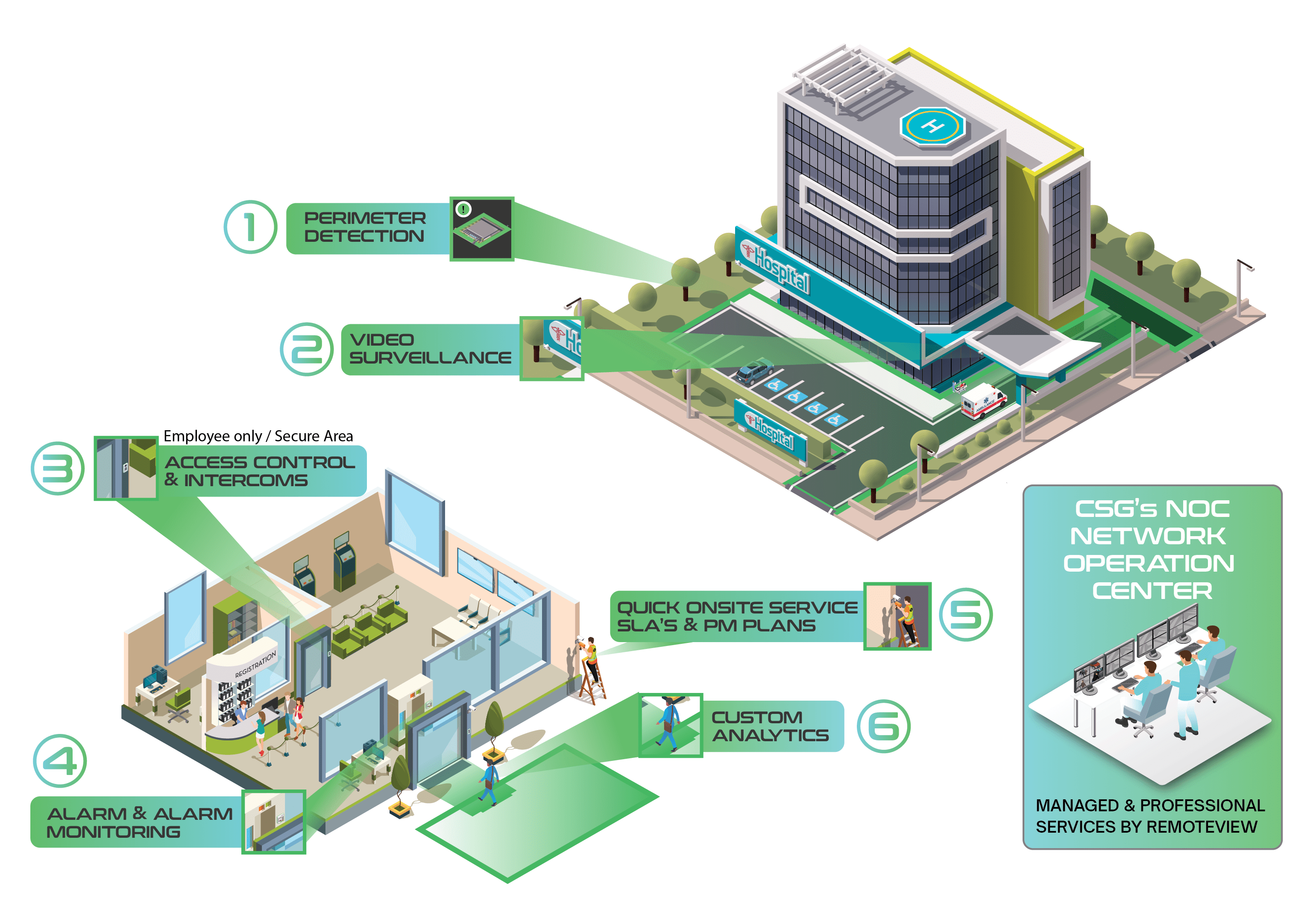

Video Surveillance, Alarms, and Access Control

Security infrastructure has to protect the institution first — but it also needs to support operations. Retail and branch teams may need easy processes for incident review. Operations may need reporting. IT needs secure connectivity and manageable systems. Security needs visibility, response procedures, and audit-ready documentation. Executives need confidence that security investments support both risk reduction and operating performance. Video surveillance, access control, and alarm systems should not be treated as separate conversations if they are part of the same branch or facility strategy.

Managed Services and Remote Support

Managed services can reduce the burden on internal teams when the scope, expectations, and reporting are clear. The institution should define what can be resolved remotely, when on-site dispatch is required, how service history is tracked, who reviews recurring issues, which systems need preventative maintenance, how uptime is reported, and what internal teams should no longer have to manage alone. Managed services are most valuable when they are part of the operating model, not just a support contract.

Vendor Consolidation

Vendor consolidation should not be approached as a blanket reduction exercise. The goal is not simply fewer partners — it's reduced complexity, improved accountability, and a more manageable institution. A good vendor consolidation discussion asks:

- Where do responsibilities overlap?

- Which vendors support multiple parts of the institution?

- Which partners understand both banking operations and security infrastructure?

- Where are service handoffs unclear?

- Which contracts create unnecessary administrative work?

- Which systems could be connected, monitored, or managed more effectively?

- Which relationships are strategic and which are purely transactional?

The right partner can help reduce friction across departments.

Questions to Ask Before Buying Another Tool

The Role of Front-Line Managers

Front-line managers are often the missing link between strategy and execution. Executives may set the direction, but managers shape the daily behavior that determines whether the strategy works. They influence staff adoption, customer guidance, workflow consistency, issue escalation, training, service expectations, and feedback.

If managers do not understand the "why" behind technology decisions, they may treat new tools as extra work instead of part of the institution's growth plan. That is especially true with branch transformation.

- If the strategy is to shift routine transactions toward self-service or assisted-service channels, managers need to know how to coach staff.

- If cash automation is meant to reduce manual work, managers need to know which workflows should change.

- If video banking is part of the service model, managers need to understand when and how customers should be introduced to it.

- If managed services are meant to reduce internal burden, managers need to know how service requests should flow.

Strategy cannot stay at the top. It has to reach the people who make daily decisions.

Why Security Should Be in the Strategy Conversation

Security is often treated as a separate track. That can create missed opportunities. For financial institutions, security infrastructure touches branch operations, employee safety, customer trust, fraud prevention, incident response, investigations, compliance, and vendor accountability. It should not be isolated from retail and operational planning.

Consider a simple branch incident. A customer dispute may require transaction records, video, employee notes, and access to system history. An ATM issue may require service logs, camera footage, and device status. A false alarm may involve branch training, alarm configuration, response procedures, and video verification. A fraud event may involve check imaging, transaction data, camera placement, customer communication, and audit documentation. Those workflows cross departments.

When security tools are integrated into operational planning, the institution can respond faster, document better, reduce noise, and improve accountability. That is why security infrastructure should be part of strategic banking technology conversations, especially when the goal is efficiency, branch transformation, or deposit growth.

How Silos Affect Deposit Growth

Deposit growth depends on operational alignment, not just marketing and product strategy. When departments plan separately, the customer experience becomes inconsistent — and inconsistency is expensive.

A customer may choose a financial institution because it is convenient, accessible, trusted, easy to use, and consistent. That experience depends on many teams working together.

- Retail defines the service model.

- IT supports the systems.

- Operations manages workflows.

- Security protects the environment.

- Facilities supports physical access.

- Vendors maintain technology.

- Branch staff deliver the experience.

- Leadership sets the direction.

If those pieces do not line up, growth gets harder. A micro-branch strategy may look attractive on paper — but to make it work, the institution needs the right mix of ITMs, video banking, cash strategy, security, access control, staffing, service hours, customer education, and remote support. If each department plans its part separately, the model may be more difficult to operate than expected.

Deposit growth needs more than a market opportunity. It needs an operating model that can support the opportunity.

How to Start Breaking Banking Silos

Breaking silos does not require every system to be replaced or every vendor relationship to change at once. Start with visibility. A practical alignment review can begin with five steps.

What Better Alignment Looks Like

A better-aligned institution does not necessarily have the newest technology. It has clearer connections between strategy, systems, people, and execution. That may look like:

- Retail and IT reviewing branch transformation plans together before vendor selection

- Operations and security using shared incident workflows

- Branch managers understanding why technology adoption matters

- ATM and ITM performance tied to customer access and branch strategy

- Cash automation measured by workflow improvement, not just equipment uptime

- Security systems supporting both risk and operational visibility

- Vendor relationships reviewed for accountability and overlap

- Managed services reducing internal burden instead of adding another layer of coordination

- Executive leadership receiving clearer feedback from the front line

- Technology investments tied to deposit growth, efficiency ratio improvement, or service delivery goals

Alignment does not remove every challenge. It gives the institution a better way to solve them.

When a Strategy Workshop Makes Sense

Cook Solutions Group's Strategy Workshops are built around the whole institution. They bring executive leadership, retail, operations, IT, security, vendor management, facilities, ATM/ITM stakeholders, and front-line management into one strategic conversation.

Our Strategic Guide for Banking Executives expands this conversation with questions around efficiency ratio, growth, micro-branches, fraud, vendors, and department alignment.

The goal is not to push one department's agenda. The goal is to see the full picture, identify where friction is slowing the institution down, and build a roadmap that can hold across departments.

Frequently Asked Questions

What is retail banking technology strategy?

Retail banking technology strategy is the plan that connects customer experience, branch delivery, digital tools, ATMs, ITMs, cash automation, security infrastructure, vendors, and IT support to the institution's business goals. It helps ensure technology decisions support growth, efficiency, service quality, and operational performance.

Why do banking departments become siloed?

Banking departments often become siloed because each team solves problems from its own perspective. Retail, IT, operations, security, vendor management, and branch teams may all make practical decisions that work locally but create complexity across the institution when they are not connected to a shared roadmap.

How do silos affect bank efficiency?

Silos can increase internal coordination, duplicate vendors, slow projects, create unclear ownership, reduce technology adoption, and add support burden for IT and operations teams. These issues can raise cost-to-serve and make it harder to improve efficiency ratio.

Why should IT be involved in retail banking strategy?

IT should be involved because retail technology depends on secure, reliable, and manageable infrastructure. ATM and ITM deployments, cash automation, digital video banking, branch systems, access control, and vendor platforms all affect connectivity, integrations, support, cybersecurity, and long-term maintenance.

How can banks reduce vendor sprawl?

Banks can reduce vendor sprawl by mapping current vendors, identifying overlap, reviewing service responsibilities, clarifying ownership, measuring internal support burden, and consolidating where one partner can support multiple connected needs without reducing performance or accountability.

How can a Strategy Workshop help align departments?

A Strategy Workshop brings leadership, retail, operations, IT, security, vendor management, and branch stakeholders into one conversation. It helps the institution identify where goals are misaligned, where technology creates friction, and which projects should be prioritized to support efficiency, growth, and execution.

.png)