What you'll find in this article:

A micro-branch is a smaller, technology-supported banking location built around a focused service model rather than transaction volume. It uses ITMs, cash automation, universal bankers, and remote support to give community banks and credit unions a lower-overhead path to deposit growth, market expansion, and relationship-based banking — without the capital commitment of a traditional full-service branch.

This article covers: what micro-branches are, how they support deposit growth, where they make sense, what technology they require, common planning mistakes, and how to measure success.

If you've worked through our strategic guide for banking executives, you know that branch expansion risk is one of the ten questions worth answering before your next planning conversation. The question isn't whether to grow, it's how much capital, overhead, and operational complexity you can afford to carry while doing it.

That's where micro-branch strategy enters the conversation.

Effective deposit growth is not just a marketing challenge. It's a delivery challenge. A bank or credit union can have strong products, competitive rates, community trust, and a clear growth goal, and still struggle to expand deposits if its physical presence, staffing model, technology, and service channels aren't aligned.

A micro-branch is not simply a smaller version of a traditional branch. At its best, it's a focused service model built around access, efficiency, relationship-building, and lower overhead. It gives financial institutions a way to test markets, support deposit growth, maintain human connection, and use technology to reduce the cost of physical expansion, without the capital commitment that stalls many institutions before they start.

For many institutions, the question is no longer whether branches still matter. The better question is: what kind of branch presence makes sense for the market, the customer, the staff, and the institution's long-term strategy?

Why Branch Strategy Is Changing

Traditional branches were built around a different banking model.

Customers visited branches for routine deposits, withdrawals, account service, loan conversations, cash handling, and problem resolution. Branches carried more of the daily transaction load because there were fewer alternatives.

That has changed.

Many routine transactions now happen through mobile banking, online banking, ATMs, ITMs, remote deposit capture, and other digital or self-service channels. Customers may visit branches less often, but they still value access when the need is important, personal, complicated, or relationship-based.

That creates a new branch challenge.

If a full-size branch is too expensive for a new market, a bank or credit union may avoid expansion altogether. If a location is too limited, the institution may fail to build enough trust and visibility. If the branch is staffed like an older transaction-heavy model, operating costs may stay high even as traffic changes.

The micro-branch sits in that middle space.

It gives institutions a way to keep physical presence in the strategy without carrying the full cost and complexity of a traditional branch model.

What Is a Micro-Branch?

Are micro-branches only for community banks or large institutions? Neither exclusively. Micro-branches are particularly well-suited for community banks and credit unions because they allow smaller institutions to test new markets, serve specific employer groups or communities, and maintain physical presence without the cost structure of a traditional branch. The model scales to the institution’s goals, not its asset size.

A micro-branch is a smaller, technology-supported banking location built around focused service delivery.

It may be used to enter a new market, serve an employer group, support a community partnership, replace an oversized branch, or create a more flexible service point in an area where a full branch does not make financial sense.

The exact model depends on the institution’s goals and overarching bank branch strategy or credit union branch strategy.

Some micro-branches are built for deposit acquisition. Some are built for advisory conversations. Some are built to serve members or customers inside a workplace or community setting. Some are designed to extend service hours with ITMs. Others are used as a test location before committing to a larger investment.

The important point is this: a micro-branch should not be designed around square footage first. It should be designed around purpose.

Traditional vs. Micro-Branch Comparison

The Fundamentals of Modern Bank Branch Design

Modern bank branch design focuses on high-impact physical layouts that prioritize open, welcoming environments over traditional barrier-heavy teller lines. A core component of this shift is the “universal banker” model, where staff are trained to handle a wide range of needs—from simple transactions to complex advisory services—anywhere in the branch. This eliminates the need for separate service desks and creates a more fluid, customer-centric experience.

The Strategic Case for Going Smaller

Micro-branches reduce overhead while preserving or improving market access — making physical expansion financially realistic for institutions that can’t justify a full branch buildout.

The real value of a micro-branch comes from its ability to reduce overhead while preserving or improving access. By optimizing the bank branch footprint, institutions can grow deposits without committing to the excessive cost and staffing of a traditional full-service model.

For banks and credit unions watching efficiency ratios, branch overhead, and deposit competition, those questions matter.

A micro-branch can lower the risk of expansion. It can also force better planning because the institution has to define what the location is meant to do. That discipline is valuable.

Micro-Branches and Deposit Growth

A micro-branch supports deposit growth by creating local visibility, enabling relationship-focused staffing, and expanding market access without proportionally expanding operating costs. Here’s how each mechanism works.

It Creates Local Visibility

Even as digital banking grows, physical presence still helps build familiarity and trust. A location in the right market can make the institution feel more accessible, especially for customers or members who want a local relationship. A micro-branch can give the institution a visible foothold without the same level of overhead as a larger branch.

It Expands Access Without Expanding Complexity at the Same Rate

A full branch can be expensive to build, staff, secure, maintain, and support. A micro-branch gives the institution another option. The right model can increase access in a target market while keeping staffing, cash handling, and facility needs more manageable. That can make deposit growth efforts more financially realistic.

It Helps Test Markets Before Larger Investment

A micro-branch can function as a market test. If the location performs well, the institution may decide to expand services, add staff, deepen community partnerships, or eventually build a larger branch. If the market does not perform as expected, the institution has limited its exposure compared to a traditional buildout. That flexibility is especially useful when leadership wants to grow but does not want to overcommit capital too early.

It Can Support Underserved or Specialized Markets

Some markets need presence, but not necessarily a traditional branch. That may include:

- Employer campuses

- Rural communities

- College environments

- Healthcare campuses

- Industrial areas

- Growing residential corridors

- Community partnership spaces

- Small business districts

- Markets where the institution has brand awareness but limited physical access

A micro-branch can be tailored to the setting. The model should follow the market.

Where Micro-Branches Make Sense

Micro-branches are not right for every location. They work best when the market and small bank branch design fit the smaller format.

New Market Entry

A micro-branch can help a bank or credit union enter a new market without the cost and risk of opening a full branch immediately. This is useful when leadership sees deposit potential but wants to test customer behavior, traffic patterns, local partnerships, and staffing needs before committing to a larger footprint.

Deposit-Focused Expansion

Some locations are not meant to handle every banking need. They are designed to create visibility, build relationships, open accounts, and support deposit growth. In this model, the micro-branch should be measured less like a traditional transaction center and more like a growth channel.

Replacing an Oversized Branch

If a full branch no longer matches customer behavior, a micro-branch may help preserve local presence while reducing overhead. This can be useful when a market still matters, but transaction volume, staffing requirements, or facility costs no longer support the older model.

Workplace or Employer-Based Banking

Some credit unions and community banks use smaller locations to serve employer groups or partner organizations. This model can be valuable when the institution has a concentrated audience and a clear relationship opportunity. The branch does not need to serve everyone. It needs to serve the right people well.

Advisory-First Service Models

Some micro-branches are built less around transactions and more around conversations. In this model, staff may focus on account openings, financial education, business services, lending referrals, or member guidance. Routine transaction access can be supported through ATMs, ITMs, digital banking, or video banking.

Markets Where Full Branch Economics Do Not Work

Some communities may need better access, but a traditional branch may not make sense financially. A micro-branch can give the institution a way to serve the area with a lighter operating model, especially when paired with strong remote support and self-service technology.

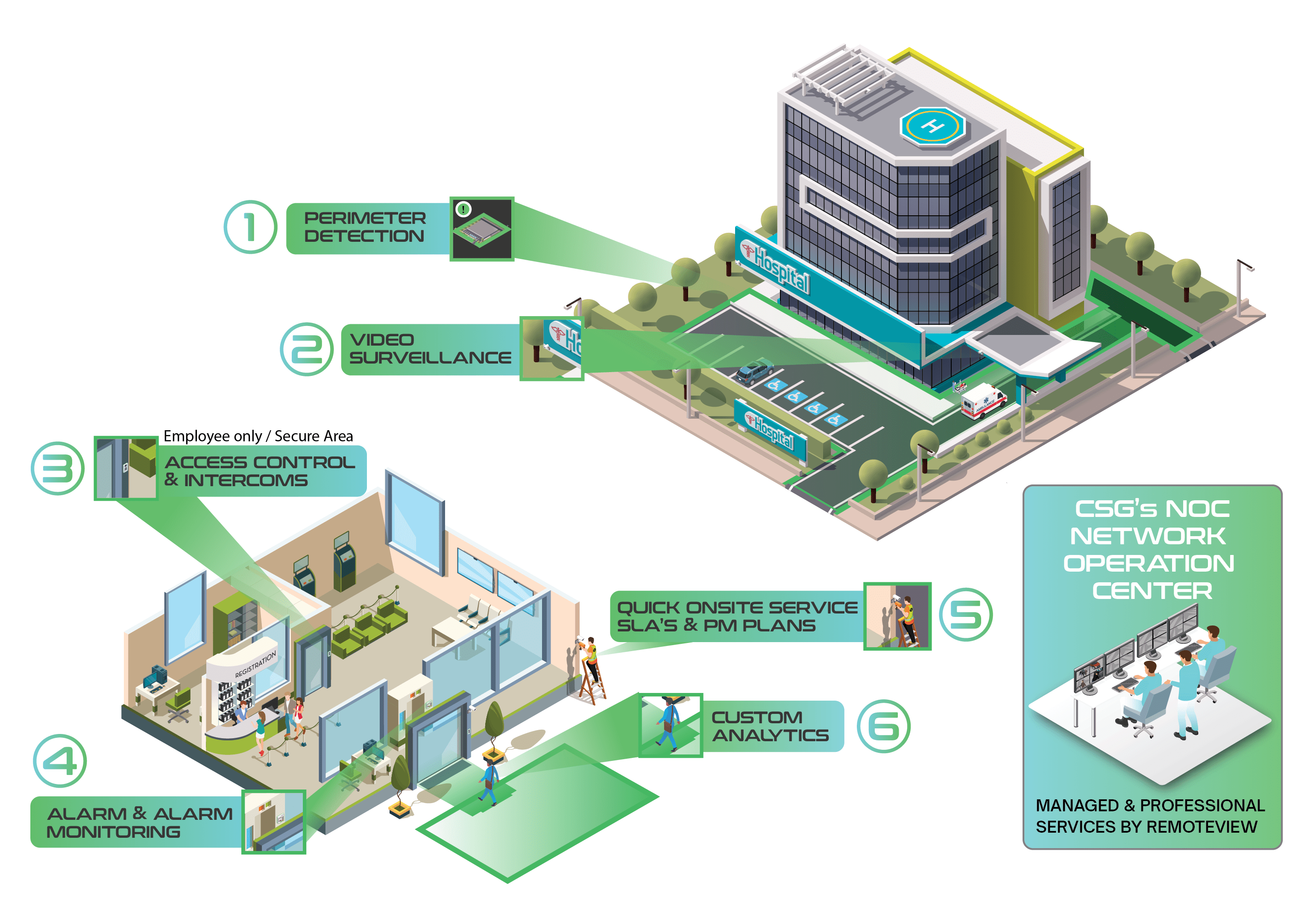

The Technology Behind a Strong Micro-Branch Model

A strong micro-branch typically combines ITMs or ATMs for transaction access, cash automation for operational efficiency, video banking for remote expertise, and managed services for uptime and support. Technology reduces friction — it doesn’t replace the service model.

Cash Automation

Cash automation can help smaller teams manage branch operations more efficiently. TCRs, cash recyclers, counters, and related tools can reduce manual handling, improve controls, and shorten routine cash processes. In a micro-branch, this matters because there may be fewer staff members available to absorb manual work.

Cash strategy should be planned early. Leadership should review expected cash volume, staffing, balancing routines, dual control requirements, branch layout, security, service needs, and support expectations.

Digital Video Banking

Digital video banking can extend the expertise available inside a micro-branch. A smaller location may not have every specialist on-site. Video banking can connect customers or members to remote experts for more complex needs, depending on the institution’s service model. The key is to make the experience feel intentional. Video banking should not feel like a backup plan. It should be built into the customer journey with clear placement, privacy, staff guidance, and support.

Digital Signage and Customer Education

Micro-branches often need to communicate quickly. Digital signage can help explain service options, promote deposit products, guide users toward ITMs or video banking, and reinforce the institution’s brand. The content should be useful, not just promotional.

Access Control, Alarms, and Video Surveillance

A smaller location still needs serious security planning. Access control, alarm systems, video surveillance, camera placement, video verification, and monitoring should be designed around the branch layout, cash-handling strategy, staff coverage, hours, vestibule access, and after-hours activity. Security should be planned with the service model, not added after the layout is complete.

Managed Services and Remote Support

A micro-branch should not depend on branch staff to troubleshoot every technology issue. Remote monitoring, service visibility, preventative maintenance, and clear escalation workflows can reduce downtime and reduce the internal burden on IT and operations teams. Comprehensive visibility is provided by the Cook Command Center. Uptime is not just a technical metric. It affects trust, adoption, and the customer experience.

Micro-Branch Planning Questions

Before launching a micro-branch, leadership should answer a set of practical questions.

What Is the Primary Goal?

A micro-branch can support many goals, but one goal should lead. Possible goals include:

- Deposit growth

- Market entry

- Member or customer access

- Employer group service

- Branch replacement

- Advisory banking

- Small business relationship growth

- Lower cost-to-serve

- Extended service availability

- Community presence

If the primary goal is unclear, the branch design will drift.

Who Is the Branch For?

A micro-branch should be designed around a defined audience.That may be existing customers, new households, employees at a partner organization, small business owners, students, rural members, or people in a growing residential corridor. The audience affects location, hours, technology, staffing, security, signage, and success metrics.

What Work Should Staff Do?

This is one of the most important questions. If staff spend most of their time processing routine transactions, the micro-branch may not create the efficiency benefit leadership expected. Define how staff should spend their time before the branch opens. For example:

- Welcoming and guiding customers

- Opening accounts

- Supporting deposit growth

- Coaching digital and ITM adoption

- Building relationships

- Identifying financial needs

- Connecting customers with remote experts

- Solving complex service issues

- Supporting small business relationships

A micro-branch succeeds when staff roles match the branch purpose.

Which Transactions Should Move to Technology?

Do not assume customers will automatically use ITMs, ATMs, or digital tools because they are available. The institution needs an adoption plan. Staff should know how to guide customers. Signage should help. The branch layout should make the right path obvious. Managers should review usage. Leadership should measure whether transaction migration is happening. Technology adoption is not only a customer behavior issue. It is also a staff coaching issue.

What Support Model Is Needed?

A smaller branch needs clear support. Before launch, define:

- Who supports the ITM or ATM?

- Who supports cash automation?

- Who monitors device uptime?

- Who handles service calls?

- Who reviews recurring problems?

- Who manages alarms and video verification?

- Who supports network or connectivity issues?

- Who tracks service history?

- Who reports performance to leadership?

Without a clear support model, a micro-branch can push extra work onto IT, operations, and branch teams.

How Will Security Work in the Space?

Micro-branch security should be designed around the actual layout and workflow. Review:

- Entrances and exits

- Staff-only areas

- Cash handling points

- Customer waiting areas

- ITM or ATM placement

- After-hours access

- Shared facility issues

- Camera coverage

- Alarm zones

- Access control permissions

- Incident response

- Video retention

- Remote monitoring needs

A smaller branch should not mean a weaker security plan.

What Does Success Look Like?

Micro-branch success should be measured differently than traditional branch success. A traditional branch may be judged heavily by transaction volume and overall production. A micro-branch may need a more focused scorecard tied to its purpose. Possible metrics include:

- Deposit growth

- New accounts

- New households or members

- Cost-to-serve

- ITM or ATM adoption

- Transaction migration

- Staff time shifted to advisory work

- Appointment volume

- Small business relationships

- Service uptime

- Customer satisfaction

- Referral activity

- Digital banking adoption

- Cash handling efficiency

- Support tickets

- Repeat service issues

The institution should define the scorecard before opening.

Common Mistakes in Micro-Branch Planning

A micro-branch is not automatically efficient. Poor planning can make a smaller location harder to operate than expected.

How Micro-Branches Affect Efficiency Ratio

Micro-branches can support efficiency ratio improvement, but only when they reduce operating drag.

The efficiency benefit may come from:

- Lower facility cost

- Reduced staffing requirements

- More focused staff roles

- Better use of ITMs and ATMs

- Less manual cash handling

- Stronger transaction migration

- Remote support and monitoring

- Better vendor accountability

- Fewer unnecessary service calls

- Faster issue resolution

- Reduced internal IT burden

- More targeted growth investment

A micro-branch should not simply lower cost. It should create a healthier relationship between cost, service, and growth.

That is why the model should be planned through both a growth lens and an operational lens.

The branch needs to help the institution reach the market, serve people well, and operate with less friction.

Micro-Branches and the Role of Human Service

The goal of a micro-branch is not to remove people from banking.

The goal is to use people better.

Customers and members may not need a teller for every routine transaction, but they still value human help when a decision matters. Opening an account, solving a complex issue, discussing a loan, planning a business relationship, or understanding financial options often requires trust.

A micro-branch can protect that human connection by using technology to reduce routine work.

That shift matters.

Staff should not be stuck behind processes that machines, remote experts, or digital tools can handle. They should be available for the conversations that build loyalty, deepen relationships, and support deposit growth.

A good micro-branch makes human service more focused, not less important.

Micro-Branch Strategy and Vendor Alignment

A micro-branch brings multiple systems together in a smaller environment.

That may include ITMs, ATMs, TCRs, cash recyclers, video banking, digital signage, alarms, access control, video surveillance, remote monitoring, service portals, and vendor platforms.

If each system is planned separately, the institution may create unnecessary complexity.

Vendor alignment matters because smaller branches have less room for operational confusion. When something breaks, staff need a clear path. When leadership wants performance data, the right information needs to be available. When IT is asked to support the environment, responsibilities need to be defined.

This is where Cook Solutions Group’s “one hand to shake” philosophy fits the conversation.

The more connected the branch model becomes, the more important accountability becomes.

A micro-branch should be simple for customers and manageable for the institution.

Building a Micro-Branch Scorecard

Before opening a micro-branch, define how you’ll measure whether it’s working. The right scorecard is built around the location’s purpose — not borrowed from how you measure a traditional branch.

A practical scorecard covers four categories:

When a Micro-Branch Is Not the Right Answer

Micro-branches are useful, but they are not the answer for every market.

A micro-branch may not be right if:

- The market requires a full-service lending or business banking center

- Expected transaction volume is too high for the model

- Cash needs are too complex

- The institution lacks a support model for the technology

- Staff are not trained for universal or advisory roles

- The location creates security issues that cannot be solved well

- The brand needs a larger presence to compete in that market

- Leadership has not defined the purpose of the branch

Sometimes the better answer is a full branch.

Sometimes it is an ITM-only location.

Sometimes it is a mobile branch.

Sometimes it is stronger digital banking.

Sometimes it is a partnership location.

Sometimes it is no physical presence yet.

The point is not to force the micro-branch model. The point is to make branch decisions based on strategy, not habit.

What to Review Before Moving Forward

If your bank or credit union is considering a micro-branch, start with a structured review.

Bring the right teams together and discuss:

- Market opportunity

- Deposit potential

- Competitive presence

- Branch traffic patterns

- Customer or member expectations

- Staffing model

- ITM and ATM strategy

- Cash automation needs

- Digital video banking use cases

- Security design

- Access control

- Alarm monitoring

- Video surveillance

- Remote support

- Vendor ownership

- IT burden

- Service expectations

- Success metrics

- Timeline and budget

- Expansion or exit criteria

This conversation should happen before the location, layout, or technology list is finalized.

When the strategy comes first, the branch model becomes easier to design.

How a Strategy Workshop Can Help

A micro-branch is not just a facilities project. It touches retail strategy, deposit growth, IT infrastructure, operations, staffing, security, service, vendor management, and customer experience. That is why micro-branch planning belongs in a broader strategic conversation.

Cook Solutions Group’s Strategy Workshops help banks and credit unions evaluate whether their branch strategy, technology, vendors, and daily operations are aligned with their growth goals. For micro-branch planning, that may include questions like:

- Where should physical presence support deposit growth?

- Could a lower-overhead model reduce expansion risk?

- Are ATMs, ITMs, and cash automation tools being used strategically?

- How should staff time shift from transactions to relationships?

- What technology is needed to support the model?

- How will uptime and service be managed?

- What security infrastructure does the location require?

- Where could vendor consolidation simplify support?

- Which KPIs should leadership review after launch?

The purpose is not to push a smaller branch model where it does not fit. The purpose is to help leadership see whether a micro-branch, ITM-supported location, hybrid service model, or traditional branch makes the most sense for the institution’s goals.

.png)